Get in touch

The Q3 unverified recycling figures released by the Environment Agency indicate another strong performance quarter.

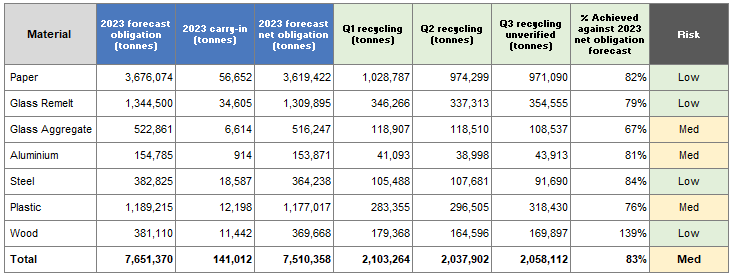

The table below shows recycling evidence requirements for 2023. It also shows the carry in tonnage reported earlier in the year from 2022. Carry in is the number of PRNs produced in December 2022 that are issued for 2023 use.

This gives us a net obligation for 2023. We can then see the Q1 and Q2 verified and Q3 unverified data for 2023. Although Q3 is not a record quarter, it is still a strong performing one, and the correction in PRN pricing across many materials has not caused a massive reduction in PRN generation.

What does this mean for producers?

The unverified Q3 2023 data has benefited from the ongoing strong performance of the recycling industry, which started in Q4 2022. Looking forward, the industry now needs to continue to perform well throughout the year to produce enough PRNs in 2023. The challenge may come not from the strong performance of recycling, but in any uplift in obligation from late submission by producers.

Medium risk

Aluminium

Aluminium has produced a record quarter, and based on these interim figures is ahead of target. This has taken the risk premium away from the PRN and the price has corrected significantly. Aluminium continues to be a packaging material of choice for consumers. In response, brand owners are switching away from plastic and glass into aluminium. There is a risk that as more companies complete the registration of their obligation, aluminium obligation will climb. This is less likely at this time of the year, however it will be keenly examined going into 2024.

Plastic

Plastic has produced a record quarter and like aluminium this has taken the risk premium away from the PRN. Recycling has missed its in-year target for the last three consecutive years, and this year could be first to exceed in year target. The price to support that level of PRN generation has been high, however given these results there has been a significant price correction. At this time in the year, it seems less likely we will see a significant late submission pushing up the obligation, however it can’t be ruled out completely.

Glass aggregate

The limited availability of glass aggregate in the market is shown in the latest data. Although this is partially driven by reduced demand for the material since Q3 2022, it is also a feature of the significant export market for glass. Regulation is expected to change in 2024, however this shortage of glass aggregate is expected to continue in 2023 and glass aggregate will undershoot the requirement for PRNs in 2023, however glass remelt is currently overperforming.

Low Risk

Glass remelt

Glass recycling volumes in Q3 continued to remain strong. Glass remelt needs to perform well in order to make up for the shortfall in glass aggregate, which continues to have low availability. The challenges in glass have continued into Q4 2023, however prices have softened in recent weeks and with lower obligation numbers we hope to see glass in balance, between obligation and PRN production.

Steel

Steel volumes in Q3 have declined however this is not a material of concern this year. Steel is a declining packaging material, and we therefore can envisage a reduction in obligation in 2023. PRN prices have continued to soften in the light of the Q3 figures.

Paper

The strong Q3 interim numbers are, once again, just below the “magic” one million, but close. This remains above market sentiment and as a consequence the PRN price has corrected further from the reduction noted on publication of Q1. However overall market trends remain unchanged, with OCC prices falling and demand for post-consumer packaging decreasing due to an overall drop in consumer spending.

Wood

Wood has achieved its recycling target for 2023, and has shown an improvement on Q2 data. There is additional pressure on ensuring volumes remain high as wood is relied on to meet the overall general recycling target. The PRN price will track against the paper PRN prices as both materials will be used to meet general recycling.

Looking ahead

Ecosurety will continue to communicate the changes in the PRN market throughout the year. The Q3 2023 data were positive overall, with most PRN prices softening as a result.

The initial obligation data shows around 300 companies still to report their obligation, so these number are understated. However a record quarter for aluminium and plastic have significantly reduced the risk of these materials producing enough PRNs in year.

If you would like to speak with Ecosurety, please contact us on 0333 4330 370.

Nigel Ransom

Head of Procurement

As Head of Procurement Nigel and his team are responsible for buying PRNs for all Ecosurety's scheme members. He undertakes market research and data analysis and makes informed decisions for the benefit of members.

Written by

Nigel Ransom

Published

07/11/2023

Topics

Latest News

Draft packaging EPR regulations sent to European Union and World Trade Organisation

By Louise Shellard 02 May 2024

European Parliament introduce regulations to improve packaging sustainability

By Louise Shellard 30 Apr 2024

Q1 2024 recycling data reveals good performance in most materials

By Nigel Ransom 29 Apr 2024